By Charlie Wilson

Part of the false propaganda about the cost of living crisis that we are being subjected to by the government is the line that there are “global headwinds” beyond their control that require the working class to get worse off; possibly indefinitely.

The “headwind” most often identified as causing the increase in the cost of energy is the war in Ukraine.

It is – however – never suggested that a better course for the UK government would be to seek to resolve and deescalate the war – so that people in Ukraine and Donbass can live in peace, and a mutual security arrangement made with Russia; to allow decreases in military spending on both sides which could be spent on solving the problems humanity has rather than adding to them.

This will be even more the case next Winter if there is no end to the war in the meantime, or sanctions are maintained as a form of self-harming pressure in the aftermath. The OECD projects that inflation will slowly subside through 2023 to 2024, but also notes that next Winter is likely to see a further spike in oil and gas prices if the war continues and also if China’s continuing economic growth raises demand for energy. This is very likely, and puts the OECD prediction in question.

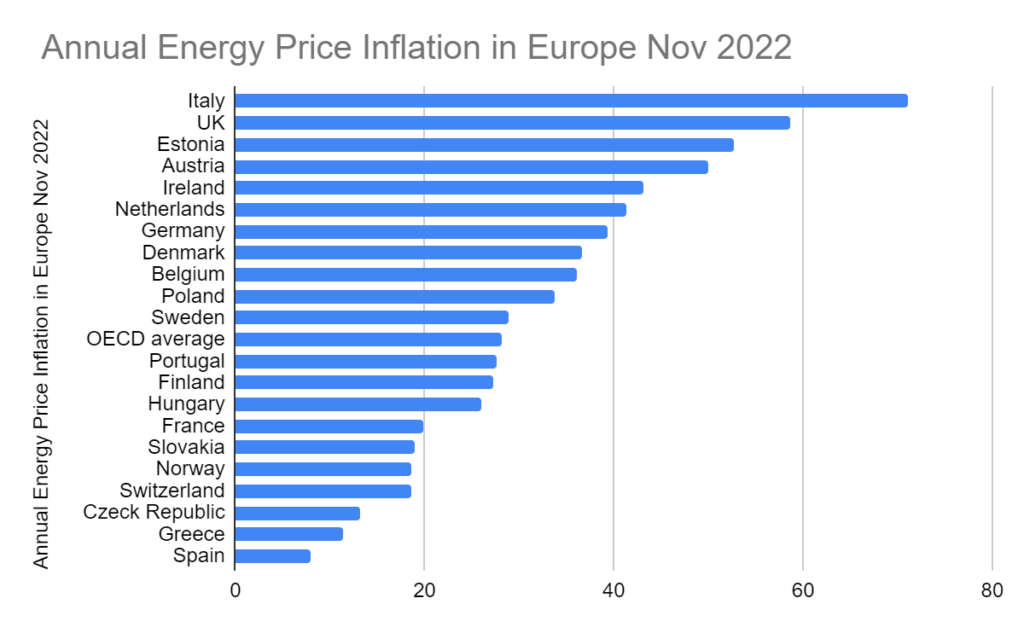

In the meantime these “global headwinds”, that the British government blames for high energy prices, seems to affect some countries far more than others, in particular the UK. As we can see from this table, there is a range of annual energy price inflation in Europe that rises from 8% for Spain to over 70% for Italy, with the UK as second worst. These figures can be further investigated and compared with other countries globally here.

See below for this in graphic terms that are easier to see at a glance. The UK energy consumer price inflation rate, in fact, is more than double the OECD average. Spain is in a particular position because it gets 90% of its gas from Algeria and is not connected up to the rest of the EU, but Germany in December 2021 got 32% of its gas from Russia compared to the UK’s 4%, so, why are prices rising so much faster here?

The UK got just 4% of its gas supply from Russia before the war, whereas Italy got 40%, which was average for the EU. At present the UK imports 50% of its gas, mostly by pipeline from Europe, but increasingly in the form of LNG, which arrives by ship from the USA, Qatar. This will increase quite quickly as North Sea production runs down; which could hit zero by 2030. It is already down to a third of what it was in 2000.

As the price of gas is set globally, regardless of where it is produced, enhanced domestic supply would have practically no impact on prices; which disposes of another myth used to try to drum up support for more North Sea gas fields or fracking. Local supply is not cheaper.

The price of gas also fixes the price of electricity, even when generated by far cheaper renewables. This is because the sources with the lowest marginal costs will be on stream all the time. This will be renewables because, once the turbines are up or the panels in place, there is no charge for the wind or sun, whereas fossil fuel plants have to pay for burning their fuel. But, although capacity is rising sharply, with six times as much as in 2010, we do not yet have enough renewable capacity to cover most of the demand most of the time. So, more expensive sources have to be brought online to fill the gaps. As the price in every half hour period is set by the marginal cost of the last generating unit to be turned off to meet demand – which is invariably a gas power plant with high marginal costs – that keeps the cost of electricity that high regardless of how it is generated. A different method of pricing to take account of the lower costs of renewables, could reduce prices and would be facilitated by public ownership of power generation.

The dizzyingly high level of energy price inflation in the UK is down to government policy choices.

As the OECD points out: “The untargeted Energy Price Guarantee announced in September 2022 by the government will increase pressure on already high inflation in the short term, requiring monetary policy to tighten more and raising debt service costs. Better targeting of measures to cushion the impact of high energy prices would lower the budgetary cost, better-preserve incentives to save energy, and reduce the pressure on demand at a time of high inflation.”

The energy price guarantee amounts to a subsidy paid to energy suppliers to avoid taxing the windfall profits of the energy producers. With these companies netting £170 billion in profits, a serious windfall tax at 100% on these, with no loopholes encouraging suicidal fossil fuel exploration, could more than meet the cost of the existing cap – £39 billion up to April 2023. If done preemptively it would cut that cost out of the inflation rate. A choice not to do this indicates that the government wants inflation to bite into the incomes of the working class as a means of levering resources up towards profits.

A better targeted measure that would meet social need and cut inflation is the TUC’s proposals for a fairer energy system which would:

- Take the Big 5 energy retailers and other failing retailers into public ownership, at a similar cost (under £2.85bn) to what Government already spent on keeping failed energy supplier Bulb in business;

- Task publicly-owned energy providers with offering a social tariff capped at 5% of income for low-income households;

- Recognise that energy is a common good: restructure tariffs to provide all households with an initial free energy allowance, and increase the cost per unit for high-consumption households.

This would:

- Protect all low-income households with fairer bills and a social tariff

- Deliver lower bills and a faster climate transition through the rapid rollout of fully-funded home energy efficiency retrofits

- Ensure that energy is a public good and that energy retail is both democratically accountable and transparent

Labour should adopt and campaign for it.

The above article was originally published here by Socialist Economic Bulletin.