By John Ross

The following article was written before the announcement of the latest US GDP figures, which showed the US economy slowing from an annualised 3.1% growth in the 1st quarter of 2019 to 2.1% in the 2nd quarter. This new data clearly confirms the analysis in the article. The Chinese version of this article originally appeared in Chinese in China Finance.

The Federal Reserve’s shift towards cutting interest rates

The US Federal Reserve’s sharp turn in summer 2019 towards cutting US interest rates immediately affects China and the global economy via numerous channels. But in addition to short-term effects, the reasons for the Federal Reserve’s policy change casts a clear light on the US economy’s medium- and long-term growth perspectives. Both aspects will affect China-US trade negotiations. This article therefore examines the fundamental growth trends in the US economy leading to the presidential election.

Why did the Federal Reserve make a sharp policy turn?

The Federal Reserve’s summer 2019 shift was an abrupt reversal of the Fed’s previous policy. During 2018 the Fed carried out four interest rate rises, clearly reflecting an estimation that the US economy had strong upward momentum and it was necessary to take prudent steps to head off overheating. Even as late as May 2019 Fed Chairman Powell said weak inflation was transitory – implying there was no reason to cut interest rates.

By June 2019, in contrast, the Federal Reserve press conference was universally interpreted as indicating the Fed would cut rates – the Fed funds futures market pricing in three quarter-point cuts in 2019, including 100% odds for a quarter-point cut this summer. A 0.25% rate cut was duly carried out at the July Fed meeting.

There are two interpretations of this radical policy change. The first is that it was a response to temporary non-fundamental trends in the US economy – short-term effects of the trade war, loss of momentum by US share markets etc. In that case the US economy may be anticipated to rapidly recover from such problems. The second interpretation is that the Fed was responding to much deeper trends slowing the US economy in 2019 – in which case the question becomes how deep is this slowing likely to be?

This difference overlaps with the fact that throughout the recent period two different perspectives for the US economy in 2019-20 have been put forward. The first, that of the Trump administration, argued that due to US tax cuts the US economy would accelerate in 2019. In March 2019, in its official budget forecasts, the administration projected 3.2% US GDP growth in 2019 and 3.1% in 2020 – both faster than 2018’s 2.9% and in line with President Trump’s claim that the US economy would grow at least 3% a year during his presidency.

The second perspective, held by the IMF, the present author, and others, was that the US economy would experience downward pressure in 2019. In that case, of course, the Fed’s policy shift was a response to deeper more powerful trends in the US economy.

Recent negative trends in the US economy

Recent US data is clearly in line with this second perspective. US total industrial production, including oil and gas, stalled after the end of 2018 – by May 2019 it was 0.9% below December 2018’s level. The decline in US manufacturing production, 1.5% in the same period, was sharper. In April 2019 US manufacturing production was 4.8% lower than its level more than 11 years previously in December 2007 – Trump’s policy to strongly revive US manufacturing production had failed.

Taking PMIs, the US Composite PMI was 51.5 in June 2019 – the second lowest since 2016. The US manufacturing PMI in the same month fell to its second lowest level since 2009 – 50.6… By the 1st quarter of 2019 the annualised growth of US fixed private investment had fallen from 9.9% when Trump was inaugurated to 1.5%.

President Trump demands the Fed cuts interest rates

These negative economic trends, in addition to direct effects, created strong political pressure on the Fed – President Trump launching a public campaign to force the Federal Reserve to cut US interest rates. The reasons for these attacks were clear. Opinion polls for Trump, leading to the official launching of his re-election campaign in June, were unfavourable. Leaks of his internal campaign polling showed the President had for several months been trailing Democrat Joe Biden. Recent polls showed President Trump trailing nine percent behind Democrat Bernie Sanders. Given negative poll ratings the prospects for the US economy in 2019-2020 were crucial for Trump’s re-election chances.

A recession in 2019?

Some major Western analysts believe that US economic slowing was so severe it indicated a US recession – two quarters of negative growth. For example, John Authers, Senior Bloomberg Editor for Markets, analysed under the self-explanatory headline ‘Markets Are Acting Like a Recession Is Unavoidable’:

‘would it be possible to explain what is going on in markets without making reference to the deteriorating U.S.-China trade relations? I am beginning to suspect that it would. Bond markets may be behaving as though they are bracing for something terrible to happen because traders are, indeed, scared that something terrible is going to happen.’

Quantitative analysis, however, indicates that any view the US economy will enter recession in 2019 is exaggerated. US growth in 2018 was 2.9%. Since the immediate aftermath of World War II, the largest deceleration in US GDP in one year compared to the previous one was 2.5% in 2009, under the impact of the international financial crisis.

However, in the 1st quarter of 2019 US GDP growth was 3.2%. For a recession to occur in 2019, between the 1stquarter and the 3rd quarter US GDP growth would have to fall from 3.2% to less than zero in only six months – a slowdown worse than during the greatest economic crisis for 80 years. Such a scale of economic deceleration is not indicated by domestic or international US economic imbalances.

Claims 2019 will see a US recession are therefore exaggerated, but there are clear reasons why the US economy will slow in 2019 and US growth will remain low in the medium/long term. This provides the background to Federal Reserve decisions.

Inaccurate claims by the Trump administration

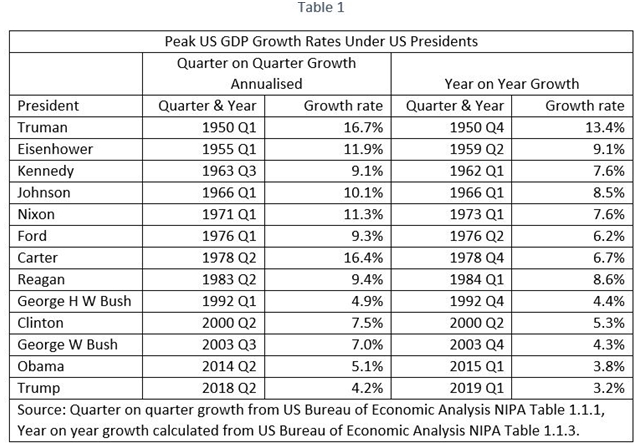

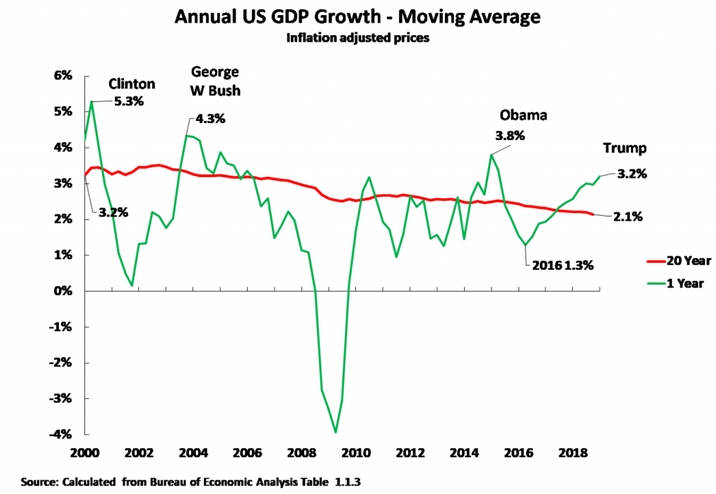

To analyse accurately US economic dynamics, merely electoral propaganda claims by the Trump administration may be dismissed. Trump has claimed that ‘America’s economy is booming like never before’ but the reality is that under President Trump the US has experienced the slowest peak economic growth during any presidency since World War II. As demonstrating this casts a clear light on fundamental US economic trends, Table 1 shows peak growth under all US Presidents since World War II presented both in the way the US publicises economic growth, one quarter’s growth compared to the previous quarter presented at an annualised rate, and China’s method of comparing a quarter in one year with the same quarter in the previous year. Both show peak economic growth under Trump is lower than under every previous post-World War II US President. Taking 21st century presidents:

- Using the US method of presenting data, peak growth under Trump of 4.2% was lower than 5.1% under Obama, George W Bush’s 7.0%, or Clinton’s 7.5%.

- Calculated using real year on year growth, 3.2% peak growth under Trump was slower than 3.8% under Obama, 4.3% under George W Bush, and 5.3% under Clinton.

But peaks under 21st century presidents were much lower than under 20th century post-World War II US presidents. For example, peak growth under Nixon was 11.3% using the US method of presenting data. Peak post-World War II growth was under Truman at 16.7% using the US method of presenting data. Slow peak growth under Trump, of course, helps explain his relatively unfavourable position in opinion polls.

The slowing of the US economy

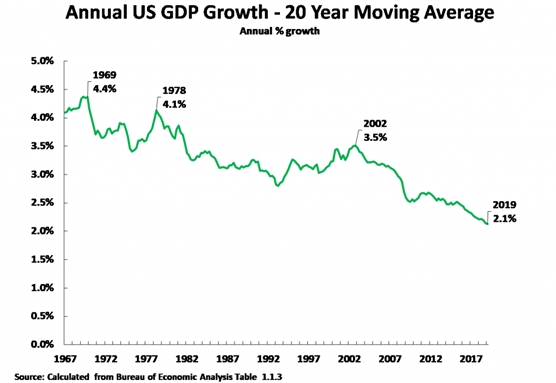

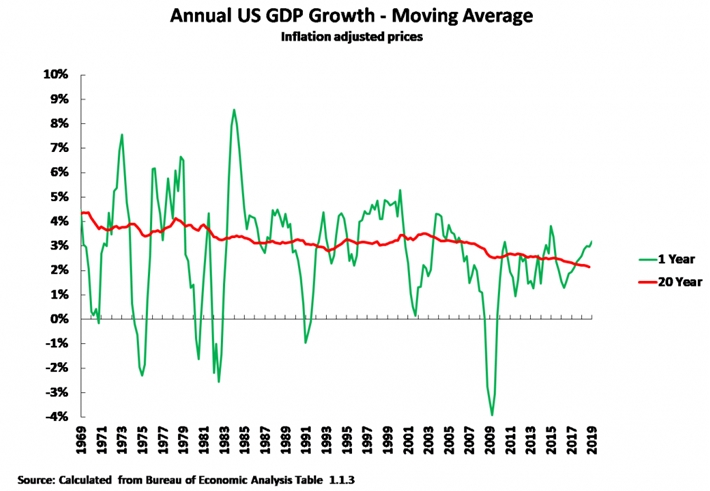

Turning to fundamental US economic trends, accurately analysing these requires distinguishing short-term business cycle fluctuations from medium/long term economic trends. The most accurate way to do this is to take a medium/long-term moving average of US growth – which eliminates effects of purely short-term fluctuations. Such measures show that taking either a 7, 10- or 20-year moving average gives the same fundamental result that long term US growth is slightly above 2% – a 7 year moving average shows annual average 2.3% GDP growth, a 10 year average shows 2.2%, and a 20 year average shows 2.1%.

Taking the longest-term moving average, 20 years, Figure 1 clearly shows that the fundamental trend of US economic growth in the last 50 years is significant deceleration. Annual average US growth fell from 4.4% in 1969, to 3.5% in 2002, to only 2.1% in 2019. In the last fifty years average annual US growth rate has fallen by more than half, explaining why US growth under Trump is the slowest under any US president since World War II but also showing that the deceleration under Trump is part of a longer-term US slowing.

This decelerating trend also demonstrates that 2.9% growth achieved by Trump in 2018, while slow by historical standards, was above current US annual average growth – with business cycle consequences analysed below.

Why is US slowdown occurring?

Given this long-term US economic slowdown, to understand US economic perspectives it is evidently crucial to analyse why this is occurring.

- One explanation ascribes deceleration merely to specific contingent events – trade wars, European economic slowdown etc. If that is correct action by the US authorities, such as Federal Reserve interest rate cuts, may prevent any slowing and create strong US medium/long term growth.

- The second explanation is that US economic slowing is due to deeper structural features. Indeed, that the US economy in 2018 grew faster than its medium/long term economic potential, and therefore the business cycle upturn in 2018 would be likely to be followed by a business cycle downturn. In that case, measures such as Federal Reserve interest rate cuts might sustain or increase US share prices, but they would be unlikely to halt downward pressures on US economic growth during 2019-2020.

To determine which perspective is correct, it is necessary to analyse the fundamental forces determining US economic dynamics.

Can Trump accelerate the US economy?

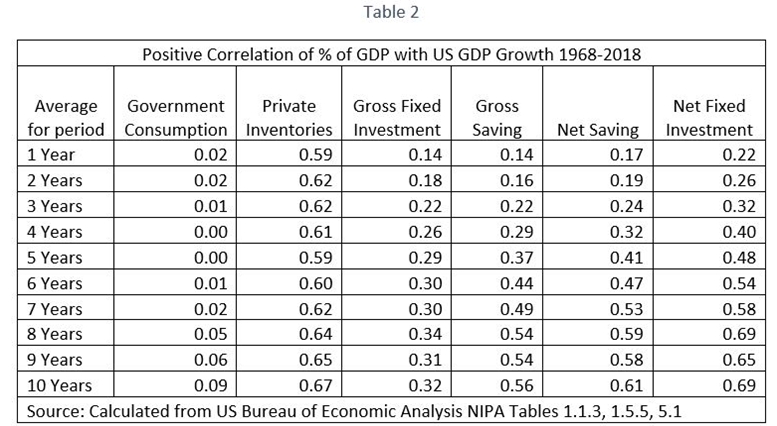

To ascertain the reasons for the US economic slowing Table 2 shows all major components of US GDP which are positively correlated with US economic growth during the last fifty years – i.e. factors which, if their structural weight in the US increased, would be expected to be accompanied by higher growth. This shows:

- US government consumption has a positive but negligible correlation with US GDP growth – the highest correlation is 0.09.

- US private inventory accumulation is strongly correlated with economic growth, but this merely reflects their strong correlation with the US business cycle. Private inventories are too small a percentage of US GDP to play a key role in US growth in anything other than the short term – in the 50 years 1968-2018 private inventory accumulation averaged only 0.4% of US GDP.

Leaving aside inventories, in the short term no component of US GDP has a strong correlation with US growth – i.e. in the short-term numerous factors affect US GDP growth with no single one playing a decisive role. Over a one to two-year period the highest correlation is only 0.26.

In the medium and long term, however, a very different picture emerges. There is a very high correlation between both US the percentage of net fixed investment (gross fixed investment minus depreciations) in GDP and net saving with GDP growth. Taking a 10-year period the correlation of the percentage of net fixed investment in US GDP with GDP growth is 0.69 – a very high correlation. Even taking a six-year period the correlation between net fixed investment and US GDP growth is 0.54.

Has Trump provided the basis for a serious US economic acceleration?

Data on the determinants of US growth, therefore, gives a clear picture:

- Medium/long term US growth is primarily determined by net fixed investment. As Qing Yuan’s article in Quishi, ‘Several Issues That Need to be Further Clarified About Sino-US trade Frictions,’ noted regarding the US economy: ‘whether it will continue to prosper depends on the state of capital accumulation,’

- In the short term no single factor is decisive in growth.

The standard caveat that correlation is not the same as causation is irrelevant in the present case – as the high correlation between US economic growth and net fixed investment means that it is impossible to substantially increase US economic growth over the medium/long term without increasing the rate of net fixed investment.

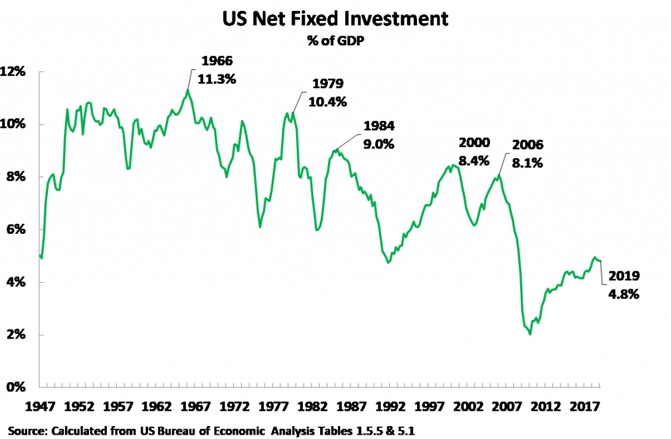

Therefore, data shows that only if President Trump could achieve a structural shift in the US economy to increase its level of net fixed investment could a substantial medium/long term US economic acceleration be achieved. But Figure 2 shows this has not occurred – US net fixed investment has fallen from 11.3% of GDP in 1966 to only 4.8% in 2019. This fall provides no basis for a medium/long term acceleration of the US economy – and this decline in net fixed investment explains the long-term deceleration of the US economy.

The state of the US business cycle

Turning from medium/long term developments to shorter-term perspectives for 2019-2020 the pattern of the US business cycle flowing from these fundamental trends is clear. Medium/long term growth, slightly over 2%, is determined by the US economy’s net fixed investment, with short-term business cycle fluctuations taking place above and below this long-term growth rate due to numerous factors. Figure 3 illustrates this short-term pattern of fluctuations. As shorter term fluctuations are simply oscillations around an average, when US growth is substantially above the average for any significant period it falls back towards the average, and when growth is substantially below the average for any significant period it then rises above the average – this process producing ‘reversion to the mean’.

Trump is experiencing a normal business cycle

These processes determine the short-term shifts in the US economy under Trump. To illustrate this Figure 4 shows year on year changes in US GDP under 21st century US presidents. This shows both the slower underlying growth of the US economy under Trump which was already analysed and fluctuations in the current business cycle. In the 2ndquarter of 2016, the US presidential election year, US growth fell to 1.3% – this extremely slow growth significantly contributing to Trump’s election victory. Such growth was far below the long-term US average – the 20-year moving average of annual average US GDP growth in 2016 was 2.4%. As 2016 was an extreme downturn of the US business cycle this was duly followed by a cyclical upturn in 2018. The increase in US growth in 2018 was not a fundamental growth acceleration but a normal cyclical upturn. It may indeed easily be verified that this upturn of the US business cycle under Trump was merely a normal business cycle one. US growth in the 2nd quarter of 2016 was 1.1% below its long-term average at that time. By the latest available data, for 1st quarter 2019, US long term growth had fallen to 2.1%. Merely to maintain a constant long-term average, therefore, a fluctuation upward of 1.1% would be expected. The 3.2% US growth in the first quarter of 2019, 1.1% above the US long term growth rate, is therefore exactly what would be expected for the peak of a normal business circle upturn – and did not represent an acceleration of medium/long term growth.

Trump’s response to economic downturn

That 3.2% year on year growth in the 1st quarter of 2019 indicates the normal expected peak growth in a US business cycle, however, has the conclusion that the beginning of a normal business cycle downturn would be expected – an undesirable development for president Trump given a presidential election in 16 months. The Trump administration will therefore do everything possible to attempt to delay this slowdown. Given that it rejects state intervention in the economy, and is already running a very large budget deficit, the only weapon available to attempt to limit an economic slowdown in the run up to the presidential election is interest rate reductions – hence President Trump’s public demand the Federal Reserve cut interest rates.

The IMF’s projections

It was shown it is unlikely there will be a US recession in 2019 but that, for business cycle reasons, the US economy will slow in 2019. Therefore, by how much will the US economy slow in 2019-2020?

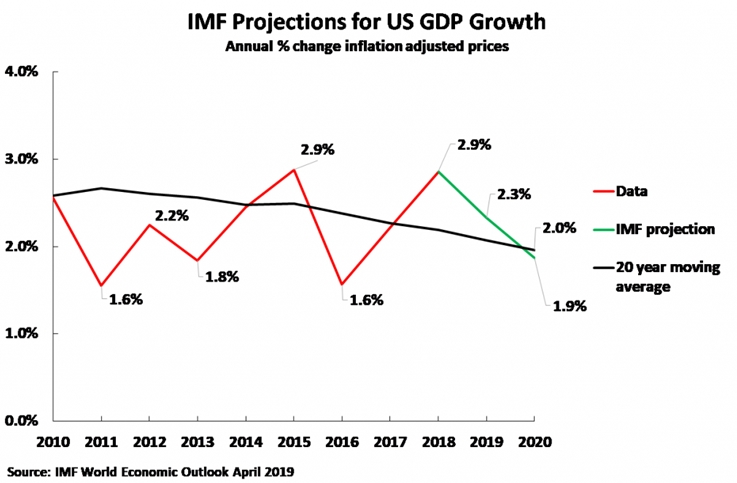

A starting point may be taken as the IMF’s projections in Figure 5, which predict a fall in US growth from 2.9% in 2018 to 2.3% in 2019 and only 1.9% in 2020. This last figure is a whole percentage point below US growth in 2018 and would represent a major economic slowdown. However, this IMF projection looks slightly pessimistic for two reasons. First, it implies that US long term growth slows to only 2.0% by 2020 – there is no indication why this should occur given that US net fixed investment is low but not falling. Second it may be assumed that President Trump will do everything possible to prevent such a sharp slowdown in an election year. For these reasons it would appear reasonable to assume a slightly higher growth figure in 2019, say 2.5% – although the IMF figure is not unreasonable. Either trend, however, indicates that the Trump administration’s claims that US growth will accelerate are false. In summary, the Trump administration will be under downward economic pressure in the period leading to the Presidential election.

Conclusion

The conclusions are therefore clear.

- The US economic upturn in 2018 was merely a normal business cycle and not any fundamental acceleration of the US economy. The long-term growth of the US economy continues to fall gradually.

- As 2018 was merely a normal business cycle upturn it will be followed by a normal business cycle downturn – that is, while not facing a recession in 2019, the Trump administration will be under pressure of a slowing economy in 2019-2020.

The abrupt change in policy by the Federal Reserve in summer 2019 was, therefore, not a response to purely peripheral or short-term factors but was a response to deep seated processes slowing the US economy.

This article was previously published on Socialist Economic Bulletin and on Learning from China.